AAPL

AAPL  MSFT

MSFT  GOOGL

GOOGL  AMZN

AMZN  TSLA

TSLA  NVDA

NVDA  META

META  JPM

JPM  V

V  JNJ

JNJ  UNH

UNH  DIS

DIS  NFLX

NFLX

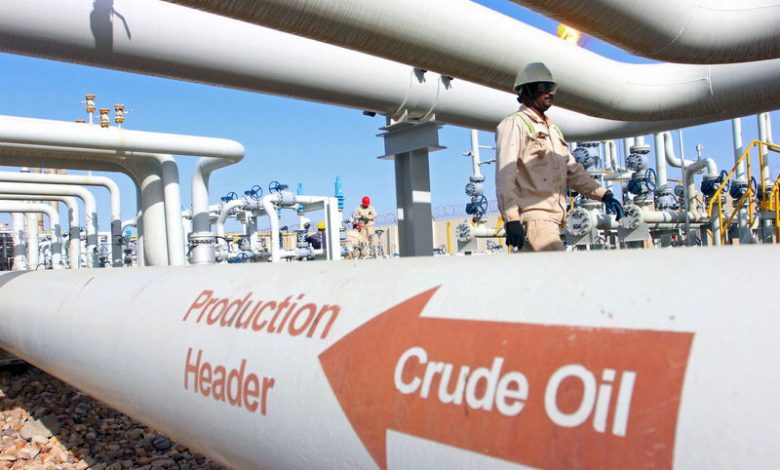

U.S. Oil Pipeline Operators Prepare for Increased Shale Production, According to Reuters

By Arathy Somasekhar

HOUSTON – Analysts anticipate that the volume of crude oil transported via pipelines from the leading U.S. shale field to export hubs on the Gulf Coast may reach pre-pandemic levels by October. This development suggests a positive turnaround for some Texas oil pipeline operators.

The COVID-19 pandemic significantly impacted pipeline construction in shale oil regions, which had previously added an export capacity of 2.5 million barrels per day from West Texas to the Gulf Coast. As oil prices plummeted in early 2020, there was an oversupply that forced pipeline companies to offer discounted deals and more favorable terms for transporting oil.

Currently, oil production in the Permian Basin of West Texas and New Mexico is on the rise, with predictions pointing to an output of 5.7 million barrels per day next year when oil prices are expected to hover around $100 per barrel. However, this output remains below the pipeline capacity of approximately 6.6 million barrels per day, according to energy research firm East Daley Capital.

The price difference, or arbitrage, between the Gulf Coast and the original point of pricing in Midland, Texas, is also expanding, indicating potential increases in shipping prices. U.S. crude oil at one terminal in East Houston for January 2023 delivery is currently trading at an 80-cent premium per barrel compared to Midland, with projections of a $1 premium by December 2023. This contrasts with a much narrower spread observed recently.

As production from the Permian Basin increases, Willie Chiang, the CEO of a major oil pipeline operator, noted that available capacity will begin to tighten, leading to more normalized tariffs for transporting oil.

One leading operator has indicated that with rising Permian outputs, it may reconsider its plans to convert one of its pipelines to transport different types of oil products instead.

Utilization of pipelines transporting oil from the Permian to the Gulf Coast is expected to rebound to around 77% of capacity by October and reach 80% by year-end, up from about 70% in April, based on estimates from East Daley Capital.

Pipeline companies typically earn significant revenue from long-term contracts with producers and refiners. During the pandemic, many major companies opted to offer more favorable contract terms and reduced rates to maintain relationships with producers rather than enforce full payments amid the downturn.

Operators are currently entering shorter-term contracts due to low price spreads but plan to transition to longer-term agreements once market conditions improve.

In terms of production indicators, the oil rig count in the Permian has increased by 14% so far this year, as reported by Baker Hughes. Many energy companies are also signaling plans to boost capital spending for the second consecutive year to add more rigs and increase output.

As AJ O’Donnell, a director at East Daley Capital, highlighted, the current landscape presents a significantly better scenario for midstream operators than just a year or two ago when the outlook was much more challenging.